Most business owners drain their bank accounts buying equipment outright. Last week, a landscaping company in Ohio wired $85,000 for a commercial mower setup—completely wiping out their operating cash reserve before summer season started.

That same owner could’ve kept $68,000 in working capital by financing 80% of the purchase. Instead, they’re now scrambling to cover payroll gaps because every dollar sits locked up in machinery.

Rate shopping matters more than most people realize. Borrowing $75,000 at 7% instead of 12% saves you $10,300 across five years. You could hire someone part-time for an entire year with that difference.

I’ve watched businesses celebrate their first approval letter, sign immediately, then discover three years later they’re paying 18% when competitors were offering 9%. Getting approved feels great. Getting approved at rates that don’t bleed your margins feels better.

How Equipment Loan Rates Work

Interest represents the annual cost of borrowing, expressed as a percentage. Different lenders calculate and present these costs in completely different formats.

Fixed Versus Variable Rate Structures

Lock in 8.5% fixed today? You’ll pay that exact rate until the loan’s paid off. Doesn’t matter if market rates explode to 12% or crater to 5% next year—you’re locked at 8.5%. Most equipment lenders prefer fixed structures since businesses need predictable payment amounts for budgeting.

Variable rates attach themselves to benchmark indexes like prime or SOFR (Secured Overnight Financing Rate). A lender quotes “prime plus 3%”—your rate adjusts whenever prime moves. Starting at 9% doesn’t guarantee you’ll finish there. Two years later, you might be paying 11%. The upside? Variable options typically start lower than equivalent fixed-rate loans.

APR Versus Factor Rates: Completely Different Math

Annual Percentage Rate combines interest plus most fees into a single yearly cost figure. At 9% APR on $50,000, you’re looking at roughly $4,500 in first-year costs (before significant principal reduction).

Factor rates use entirely different calculations, showing up mainly with merchant cash advances or very short-term agreements. You’ll see “1.25” instead of a percentage. Multiply your borrowed amount by that factor for total repayment: $50,000 × 1.25 = $62,500. Seems like 25% until you realize that’s compressed into maybe six months, which translates to true APR exceeding 35%.

Current Market Rate Ranges

In 2026, equipment financing ranges anywhere from 5% up to 30%. That’s not a typo—the spread is enormous. Where you land depends entirely on your situation. Businesses with solid credit typically land between 6% and 15%. SBA 504 programs cluster around 5.5-7% for equipment transactions, while online lenders serving startups charge 12-25%. This massive range reflects wildly different risk assessments across borrower profiles.

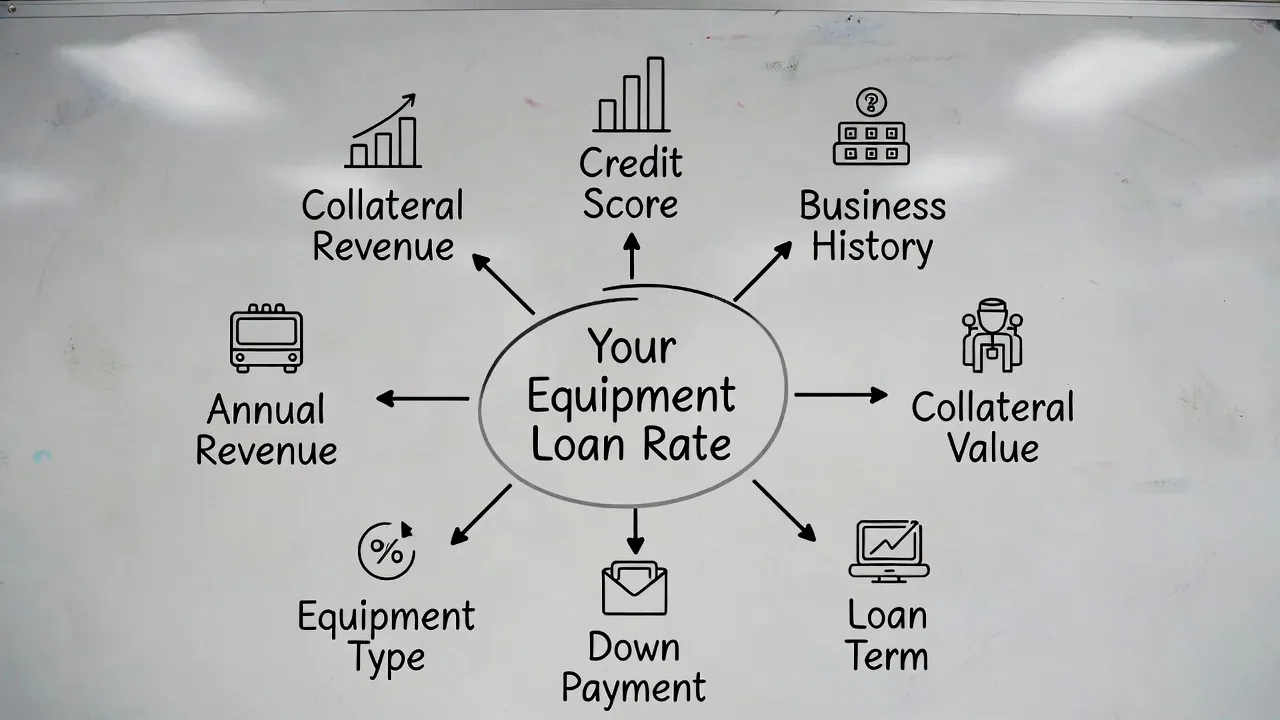

What Affects Your Equipment Loan Rate

Lenders analyze multiple factors when pricing your specific deal. Understanding these variables helps you optimize them before applying.

Credit Score and Financial History

Your credit scores—both personal and business—dominate every conversation about rates. Lenders view these numbers as predictive indicators of repayment likelihood.

Got a personal FICO above 720? You’ve unlocked the best pricing from conventional lenders. Slip into the 650-720 range? Expect rates jumping 2-4 percentage points even though you’ll still get approved. Below 650 means rates pushing 20%—or outright rejections from traditional banks.

Business credit through Dun & Bradstreet, Experian Business, or Equifax Business influences pricing for companies with track records. Strong business credit sometimes compensates for weaker personal scores, particularly if you’ve been operating five-plus years.

Recent bankruptcies, foreclosures, or tax liens spike rates dramatically when they don’t disqualify you completely. Most conventional lenders require at least 24 months of separation from major credit events before considering competitive pricing.

Equipment Type and Value

Whatever you’re buying becomes the collateral. That makes the equipment itself crucial to how lenders price your deal.

Equipment with robust resale markets receives better pricing. Standard forklifts or commercial delivery trucks qualify for lower rates than specialized laboratory equipment with three buyers nationwide. Medical devices, construction machinery, and IT hardware typically secure favorable rates because repossessing and reselling them presents minimal challenges.

Brand-new equipment consistently beats used on rates. A 2026-model excavator might qualify at 7% while an identical 2021 version gets quoted 10% since depreciation has eroded collateral value.

Loan-to-value ratios significantly impact pricing. Borrowing $40,000 against $50,000 equipment (80% LTV) costs less than financing $48,000 of identical gear (96% LTV). Lower lender exposure equals better rates.

Loan Term and Down Payment

Longer terms extend lender risk exposure, increasing rates. A 36-month deal might run 8% while stretching identical financing to 60 months bumps rates to 9.5%.

Down payments reduce lender risk while demonstrating financial commitment. Putting 20% down frequently cuts rates by 1-2 points compared with zero-down financing. Smaller borrowed amounts mean less interest regardless of rate.

Many lenders tier their pricing: 0-10% down triggers standard rates, 10-20% down earns quarter-point reductions, and 20%+ down unlocks preferred pricing.

Average Rates by Lender Type

Different lender categories target distinct market segments with varying rate structures.

| Lender Category | Rate Range | Financing Amounts | Term Length | Speed to Funding | Ideal Borrower Profile |

|---|---|---|---|---|---|

| Banks | 6-12% | $50K-$5M | 3-7 years | 2-6 weeks | Established businesses, strong credit |

| Credit Unions | 5.5-10% | $25K-$500K | 3-5 years | 1-4 weeks | Members, community-based businesses |

| Online Platforms | 8-25% | $5K-$500K | 1-5 years | 1-3 days | Newer operations, urgent needs |

| Specialized Equipment Financiers | 7-18% | $10K-$2M | 2-7 years | 3-10 days | Industry-specific purchases |

| SBA-Approved Lenders | 5.5-9% | $50K-$5M | 5-10 years | 4-8 weeks | Long-term assets, patient borrowers |

Banks offer the lowest rates but enforce strict qualification requirements. You’ll need two years in business, annual revenue exceeding $250,000, and personal credit above 680. They’re slow but build relationships extending beyond single transactions.

Credit Unions undercut bank rates by half to one full percentage point thanks to nonprofit status. Membership requirements apply—employment, geographic location, or association affiliations usually determine eligibility. They excel at deals under $250,000.

Online Platforms sacrifice rate competitiveness for speed and accessibility. They’ll fund six-month-old businesses with 600 credit scores. Same-day approvals and minimal paperwork cost you 3-10 percentage points above traditional options.

Specialized Equipment Financiers concentrate on specific verticals like construction, transportation, or medical. Industry expertise accelerates approvals and increases funding odds. Pricing falls between banks and online lenders.

SBA-Approved Lenders process government-backed loans featuring extended repayment terms. The 504 program specifically targets equipment and real estate at rates running 2-4 points below conventional alternatives. You’ll exchange extensive documentation requirements and slower processing for substantial savings.

Business owners consistently underestimate credit profile impact on equipment financing rates. I’ve watched identical businesses with similar revenue and operating time receive rate quotes differing by five percentage points solely because one owner carried a 720 credit score while the other sat at 650. That gap costs tens of thousands over five-year financing. Three months spent improving credit before applying frequently saves more money than twelve months of aggressive rate shopping.

Jennifer Martinez

Requirements to Qualify for Better Rates

Lenders establish minimum thresholds, but exceeding them significantly improves pricing.

Credit Benchmarks

Premium pricing requires personal FICO scores at 700 minimum. Business credit above 75 (on 100-point scales) benefits companies with history. Recent payment performance carries more weight than problems from three years ago.

Pull credit reports three months early. Dispute errors and reduce revolving balances below 30% of limits before lenders run checks.

Operating History

Most banks want you operating at least two years before they’ll consider you. Exceptional credit sometimes gets newer businesses approved, but don’t count on it. Hit year three? That’s when top-tier pricing opens up. Under twelve months? You’re rarely qualifying below 15% without substantial down payments or additional collateral backing the deal.

Revenue Requirements

Lenders set different thresholds depending on how much you want and who you’re asking. Banks commonly require revenue reaching 3-4 times annual debt service. For $50,000 financed with $1,200 monthly payments ($14,400 yearly), expect minimum revenue requirements around $150,000-$200,000.

Higher revenue relative to loan size demonstrates repayment capacity and reduces perceived lender risk, improving rates.

Documentation Requirements

Complete, organized documentation accelerates approvals and projects professionalism influencing pricing decisions. Standard packages include:

- Business tax returns (two years)

- Personal returns for owners with 20%+ equity

- Current year profit and loss statement

- Balance sheet

- Bank statements (three to six months)

- Equipment quote or purchase invoice

- Formation documents and licenses

Certain lenders request customer contracts, accounts receivable aging reports, or industry certifications depending on business type.

Collateral Beyond the Equipment

Purchased equipment serves as primary collateral, but additional security improves rates. Blanket liens on other business assets or personal guarantees backed by home equity sometimes reduce rates half to one-and-a-half points.

Lenders also evaluate equipment lifespan. Financing a $100,000 machine with fifteen-year useful life over five years presents less risk than financing seven-year equipment over six years.

How to Compare and Apply for Equipment Financing

Structured approaches prevent costly mistakes and surface optimal deals.

Step 1: Calculate Actual Needs and Payment Capacity

Figure out total equipment cost—delivery, installation, modifications, all of it. Add 10-15% padding for surprises. Calculate comfortable monthly payments by analyzing cash flow—never commit to payments consuming more than 15-20% of monthly revenue.

Check credit scores and scan reports for errors. Know your revenue, time in business, and debt service coverage ratio (net operating income divided by total debt payments). Anything above 1.25 shows lenders you’ve got strong repayment capability.

Step 2: Research Options and Get Prequalified

Pick four to six potential lenders across different categories. Most online platforms offer soft-pull prequalification showing estimated rates without impacting credit scores. Banks and credit unions may require hard inquiries—limit those applications strategically.

Compare total costs, not just rates—include terms, prepayment clauses, origination fees, and funding timelines. A 9% loan with zero fees beats an 8.5% loan carrying 3% origination costs in most scenarios.

Step 3: Submit Complete Applications

After identifying your top two or three options, submit full applications within fourteen days. Credit scoring models treat multiple inquiries for identical purposes within this window as single events, minimizing score damage.

Respond immediately to documentation requests. Delays signal disorganization and can trigger rate increases if market conditions shift during extended processing.

Step 4: Evaluate and Negotiate Offers

When offers arrive, compare total repayment over loan life, not monthly payments. A $50,000 loan at 9% over five years totals $62,755, while identical terms at 11% run $66,231—a $3,476 gap.

Got multiple offers? Bring competing quotes to your preferred lender. Banks sometimes match competitor pricing for qualified borrowers, particularly when additional business relationships exist.

Step 5: Close and Receive Funds

You’ll need equipment invoices or purchase agreements before final approval goes through. Some lenders pay vendors directly; others deposit funds in your account. Online platforms fund within 1-3 business days after final approval, banks take 5-10 days.

Store all loan documents and establish automatic payments to avoid late fees and credit damage.

Equipment Loan Rate Calculation Example

Real numbers illustrate rate differences clearly. Consider $50,000 equipment financed at various rates and terms.

| Rate | Term Length | Monthly Payment | Total Interest Cost | Complete Repayment |

|---|---|---|---|---|

| 6% | 3 years | $1,523 | $4,828 | $54,828 |

| 6% | 5 years | $967 | $8,000 | $58,000 |

| 10% | 3 years | $1,613 | $8,068 | $58,068 |

| 10% | 5 years | $1,062 | $13,748 | $63,748 |

| 15% | 3 years | $1,733 | $12,388 | $62,388 |

| 15% | 5 years | $1,190 | $21,399 | $71,399 |

What This Small Business Equipment Loan Rates Example Shows:

Five percentage points separating 10% from 15% on a five-year loan adds $7,651 in interest—over 15% of original borrowed amount. Even a modest two-point gap (8% versus 10%) adds $2,500-3,000 to total cost.

Extending repayment reduces monthly obligations but explodes total interest. The 15% five-year option costs $21,399 in interest versus $12,388 for the three-year version—a $9,011 difference despite identical rates.

The smallest monthly payment doesn’t automatically win. That comfortable $1,190 payment at 15% for five years carries $21,399 in interest charges. The $1,523 payment at 6% for three years costs only $4,828 in interest—you save $16,571.

Most businesses find sweet spots balancing affordable payments with reasonable total cost. Four-year terms at competitive rates often hit this balance, though cash-rich operations should choose shorter terms minimizing interest expense.

FAQs

Personal FICO scores hitting 720 or higher typically unlock premium rates from conventional lenders, usually landing in the 6-10% range. Scores between 680-720 still access competitive rates around 8-12%. Fall below 650? You’re facing rates above 15% or approval only from alternative lenders. Business credit scores exceeding 75 help established companies, though personal credit typically carries more weight for small business financing.

Absolutely—especially when you’re holding multiple offers or showing strong financials. Banks and credit unions sometimes match competitors for qualified borrowers. Online lenders typically show less flexibility since automated pricing models drive their rates. Your strongest negotiating position comes from competing offers, excellent credit, substantial down payments, or bringing additional business like operating accounts or other loans to the relationship.

Generally yes, treated as ordinary business expenses. Interest portions of equipment loan payments typically qualify as tax-deductible business expenses, lowering taxable income. Tax treatment depends on business structure and individual circumstances. Section 179 and bonus depreciation may deliver additional tax benefits for equipment purchases. Work with your accountant to maximize tax advantages and determine whether financing or cash purchase makes more sense for your tax situation.

When lenders have physical collateral securing the debt—like the actual equipment being financed—they’ll price loans more aggressively than unsecured options. Equipment-backed deals typically run 6-15% for qualified borrowers. Unsecured term loans often span 10-30% since lenders face higher risk without tangible assets to repossess if borrowers default. Equipment loans restrict funds to specific equipment purchases, while term loans offer flexibility for any business purpose. SBA loans backed by equipment frequently provide the lowest available rates, typically 5.5-9%.

Origination fees (1-5% of loan amount), documentation fees ($100-500), and application fees ($50-250) increase effective cost beyond stated rates. Some lenders charge prepayment penalties for early payoff, typically 2-5% of remaining balance. Monthly servicing fees ($10-50) accumulate over loan life. Always calculate APR including all fees to compare true costs. Ask specifically about prepayment penalties, late payment fees, and ongoing monthly charges before signing anything.

Yes, refinancing equipment loans makes sense when rates have fallen significantly since origination. However, check for prepayment penalties on your current loan—these often eliminate refinancing savings. Refinancing typically requires equipment retaining sufficient value as collateral and your business meeting current qualification standards. Most lenders want at least 1-2 percentage points rate reduction to justify refinancing after considering closing costs and fees.

Equipment loan rates directly determine whether financing makes financial sense or becomes a cash flow burden lasting years. The difference between excellent and mediocre rates on typical equipment purchases frequently exceeds $10,000 in total interest costs.

Credit profile, business financials, down payment size, and lender selection all substantially impact received rates. Businesses showing strong credit and two years of profitable operations access rates in the 6-10% zone from traditional lenders. Newer businesses or those with credit challenges pay 12-25% but can still secure financing when equipment purchases drive revenue growth justifying higher costs.

Shopping across multiple lender categories—banks, credit unions, online platforms, and equipment financing specialists—reveals true market rates for your situation. The fastest approval doesn’t automatically equal the best deal, and the lowest advertised rate may include fees making it more expensive than alternatives.

Calculate total costs across loan term, not just monthly payments. Extended terms with lower payments might cost $15,000 more in interest than shorter terms with $200 higher monthly obligations. Run calculations before committing.

Most importantly, strengthen rate positioning before applying by building credit, accumulating cash reserves for larger down payments, and organizing complete financial documentation. Three months of preparation frequently saves thousands in interest costs over loan life.