Here’s something most people don’t realize: when you make your monthly mortgage payment, there’s a good chance your local bank isn’t the one collecting that money anymore. Instead, your payment might flow to a trust in Delaware that sold bonds to a pension fund in California. That’s securitization at work.

This financial technique turns loans—mortgages, car financing, credit card balances—into tradable investment products. A lender originates thousands of loans, bundles them together, and sells ownership stakes to outside investors. The bank gets cash today instead of waiting 10 or 30 years for borrowers to pay everything back. Investors get a stream of interest payments. Borrowers? They often don’t even notice the change.

Wall Street moves about $3.5 trillion through securitized products annually in the U.S. alone. The practice keeps credit flowing through the economy, but it also introduces risks that nearly broke the global financial system in 2008. Let’s break down exactly how this works, why banks do it, and what can go wrong.

Securitization Definition and Core Concept

Securitization pools together loans or other assets that generate predictable cash flows, then sells securities backed by those payment streams to investors. The phrase “asset securitization” refers to this conversion—taking something illiquid (a 30-year mortgage sitting on a bank’s books) and making it liquid (bonds that trade on secondary markets).

Picture a small credit union in Ohio that’s approved 400 auto loans totaling $12 million. Those loans represent future income—borrowers will send in payments every month for the next five years. But the credit union needs that $12 million now to make new loans. Waiting five years isn’t practical when they want to grow.

So they gather those 400 loans into a single package, legally transfer ownership to a separate entity, and that entity issues bonds to investors. Hedge funds, insurance companies, and mutual funds buy those bonds. The credit union receives roughly $12 million upfront (minus fees and some retained risk). Borrowers keep making their payments, but now the money goes to bondholders instead of back to the credit union.

Why does any of this matter? Three reasons:

Immediate liquidity: Lenders can recycle capital faster. Make loans, sell them off, make more loans. This cycle expands how much credit flows into the economy without requiring banks to hold every loan until maturity.

Spreading risk around: One bank holding 10,000 mortgages in Florida faces concentrated geographic risk. If a hurricane devastates the region, defaults spike. Securitization lets that bank transfer Florida exposure to a global investor base.

Opening new investment channels: Pension funds and insurance companies need safe, steady returns. They can’t open bank branches and originate mortgages themselves. Securitization packages those mortgage payments into bonds they can buy, connecting institutional capital with consumer borrowers.

The first mortgage securitizations happened in the 1970s when Ginnie Mae pooled FHA loans. Banks realized they could do the same with conventional mortgages, then auto loans, then credit cards. By the 2000s, Wall Street was securitizing everything from cell tower lease payments to David Bowie’s future music royalties (yes, really—the “Bowie Bonds” of 1997).

How the Securitization Process Works

Three main steps convert a pile of individual loans into tradable securities: gathering assets, creating legal separation, and slicing up the risk.

Origination and Pooling of Assets

It starts with ordinary lending. A bank approves mortgages. An auto finance company funds car purchases. A credit card issuer extends credit lines. These loans accumulate on the lender’s balance sheet over weeks or months.

When the lender decides to securitize, they don’t just grab random loans. They select assets that share common characteristics—similar credit scores, loan sizes, geographic regions, interest rates. A mortgage pool might include only 30-year fixed-rate loans to borrowers with FICO scores between 720 and 780, all originated in the past six months, all with loan-to-value ratios under 80%.

Why such tight criteria? Investors need to model future cash flows. If every loan in the pool behaves differently, projections become guesswork. Homogeneity makes the math cleaner and the risk easier to price.

Let’s say an auto lender pools 2,000 car loans worth $50 million. Average loan: $25,000. Average term: 60 months. Average FICO: 710. The lender reviews each file to confirm the paperwork is clean—titles are clear, insurance is current, no obvious fraud red flags.

Once satisfied, the lender prepares to transfer legal ownership of those 2,000 loans out of their own hands entirely.

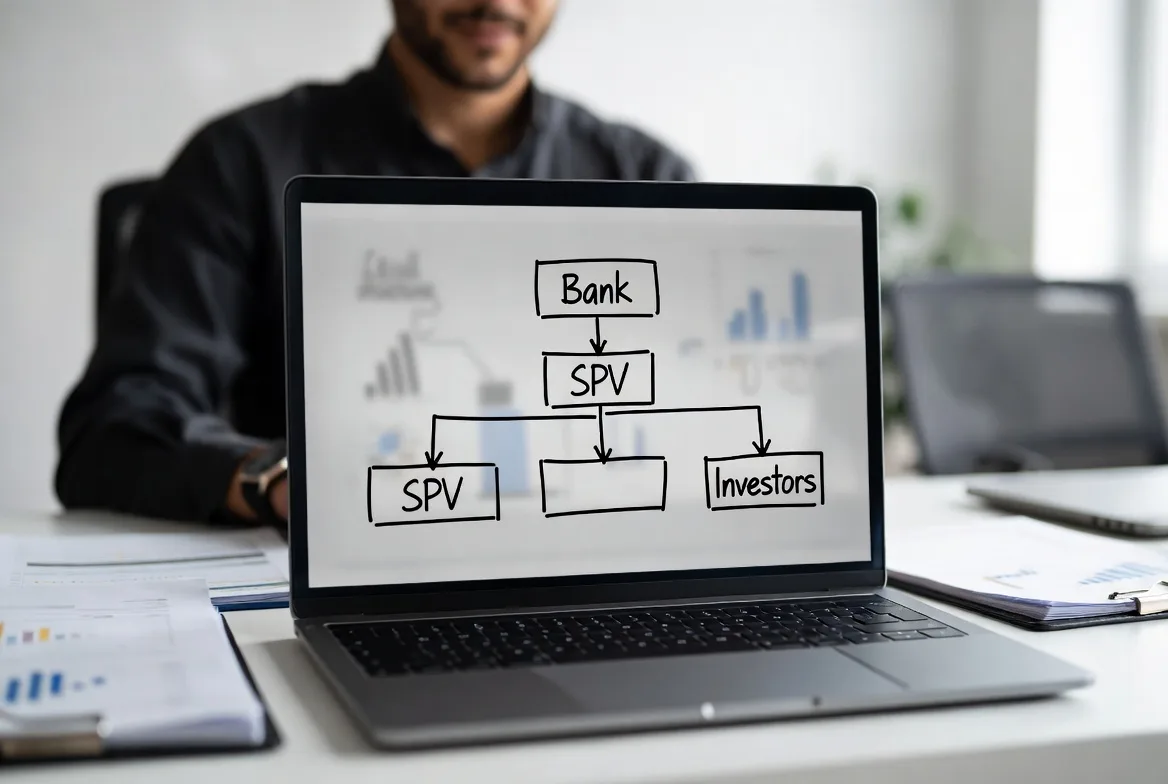

Creating Special Purpose Vehicles (SPVs)

The lender doesn’t sell directly to investors. Instead, they create a Special Purpose Vehicle—a legal entity that exists solely to hold these loans and issue bonds. Think of it as a robotic company with no employees, no office, and only one job: collect loan payments and pass them to bondholders.

Why the middleman? Bankruptcy protection. If the originating bank fails, creditors can’t raid the SPV to satisfy their claims. The loans inside the SPV are legally separated—a “true sale” that cuts all ties to the original lender’s financial health. Investors buying securities from the SPV own a piece of those cash flows directly, insulated from the bank’s other problems.

The SPV purchases the loan pool using money raised from selling bonds. A law firm writes a detailed opinion confirming the sale meets legal standards for bankruptcy remoteness. Courts have upheld these structures repeatedly, though occasional disputes still arise over whether a transfer was truly a “sale” or just a secured loan in disguise.

Two parties manage the SPV’s operations even though it has no employees:

The servicer (often the original lender) handles day-to-day administration—collecting payments, sending late notices, processing payoffs, foreclosing if necessary. They earn a servicing fee, typically 0.25% to 0.50% annually of the outstanding loan balance.

The trustee (usually a bank trust department) acts as referee. They receive money from the servicer, distribute it to bondholders according to the transaction rules, watch for violations of covenants, and represent investor interests if conflicts arise.

Issuing Securities to Investors

Now the SPV sells bonds backed by the loan pool. Most deals create multiple tranches—layers of securities with different priority rankings.

Think of it like a waterfall. Cash from borrower payments flows down from the top. The most senior tranche drinks first, taking every dollar of interest and principal it’s owed. Once that tranche is satisfied, excess cash flows to the next level down. The bottom tranche gets whatever’s left after everyone above has been paid.

A typical structure might look like this:

Class A (senior): $40 million, rated AAA, pays 4.8% interest, gets paid first.

Class B (mezzanine): $7 million, rated A, pays 6.2% interest, subordinate to Class A.

Class C (junior): $2 million, rated BBB, pays 8.5% interest, subordinate to A and B.

Equity: $1 million, not rated, receives whatever’s left over.

If borrowers default, losses hit from the bottom up. The equity tranche gets wiped out first, absorbing 100% of losses up to $1 million. After that, Class C starts taking hits. Classes A and B only lose money if defaults exceed $3 million—a 6% loss rate on the original pool.

This layering lets conservative investors buy senior tranches with minimal risk while aggressive investors chase higher yields in subordinated tranches. A pension fund managing retirees’ money buys Class A. A hedge fund seeking 12% returns buys equity.

Rating agencies—Moody’s, S&P, Fitch—analyze each tranche and assign credit ratings. They model default scenarios (what if unemployment spikes?), evaluate collateral quality, test structural protections like overcollateralization (holding $52 million in loans to back $49 million in bonds), and determine how much loss each tranche can withstand before suffering impairment.

Every month (or quarter), borrowers make payments. The servicer collects them, deducts their fee, and wires the net amount to the trustee. The trustee follows a priority waterfall spelled out in 300 pages of legal documents, distributing cash to each tranche in order until the bonds are fully repaid or the loans default.

Types of Securitization in Finance

Different asset types require different structures, but several categories dominate the market.

Mortgage-Backed Securities (MBS): Residential and commercial real estate loans. Agency MBS come from Fannie Mae, Freddie Mac, or Ginnie Mae and carry government backing (explicitly for Ginnie, implicitly for the others). Investors treat these as nearly risk-free. Non-agency or “private label” MBS have no government support—performance depends entirely on borrower credit quality and property values. These deals nearly disappeared after 2008 but have gradually returned with much tighter underwriting.

Asset-Backed Securities (ABS): Catch-all category for non-mortgage consumer debt. Auto loans are the biggest segment—Ford Credit, GM Financial, and others regularly securitize vehicle financing. Credit card ABS pool receivables from Visa, Mastercard, and Discover accounts. Student loan ABS bundle education debt (though government loans dominate that market now). Equipment leases, personal loans, even “buy now, pay later” balances show up in ABS deals. Auto loan transactions typically run 3-5 years. Credit card ABS use “revolving” structures where the SPV reinvests principal payments into new receivables for the first couple years before switching to amortization mode.

Collateralized Loan Obligations (CLOs): These securitize corporate loans—specifically, leveraged loans made to below-investment-grade companies. A CLO manager buys $400 million in loans from 100-150 different companies, pools them into an SPV, and issues tranches to investors. Unlike most securitizations, CLOs are actively managed. The manager can sell loans, buy new ones, and trade within guidelines trying to maximize returns. U.S. CLO issuance hit $125 billion in 2024, making it one of the largest securitization markets.

Collateralized Debt Obligations (CDOs): Similar to CLOs but can include bonds, other securitized products, or mixed collateral. CDOs became infamous during the financial crisis when “CDOs squared” (CDOs that owned tranches of other CDOs) amplified losses across the system. The market collapsed and remains much smaller today.

Whole Business Securitization: Cash flows from operating businesses serve as collateral. U.K. pub chains, U.S. quick-service restaurant franchisees, nursing home operators, and even Dunkin’ Donuts have securitized their revenue streams. These deals don’t pool discrete loans—they pledge future business income itself.

Esoteric ABS: The weird stuff. David Bowie securitized royalties from his back catalog in 1997, raising $55 million. Aircraft leases, lawsuit settlements, taxi medallion loans (which went badly), cell tower revenues, and solar panel leases have all been securitized at various times. Markets stay small because investors struggle to model risks they don’t understand.

Each category carries distinct risks. Mortgages correlate with housing markets and interest rates. Auto loans track employment and used car values. CLOs depend on corporate health and whether companies can refinance maturing debt. Credit card performance hinges on consumer spending and unemployment.

Benefits of Securitization for Lenders and Investors

Why bother with all this complexity? Because the benefits are substantial for both sides of the transaction.

Lenders get their capital back faster. A community bank that originates $100 million in mortgages annually ties up capital for decades if they hold those loans. Securitize them, and they can redeploy that $100 million into new mortgages every year. One bank effectively becomes five banks in terms of lending capacity.

Regulatory capital requirements drop. Basel III rules force banks to hold capital against risk-weighted assets. A commercial loan might require 8% capital backing. Securitize it with proper structure, and the bank removes it from their balance sheet entirely, freeing that capital for other uses or returning it to shareholders.

Geographic and sector concentration risks decrease. A regional bank in Texas with heavy oil-and-gas exposure faces disaster if energy prices crash. Securitizing those loans transfers the risk to a diversified investor base—a Tokyo insurance company, a London hedge fund, a New York pension fund. The Texas bank still makes the loans (they know the local market best) but doesn’t bear all the consequences if things go south.

Access to cheaper funding sources. Securitization taps institutional investors who can’t make direct loans but have trillions to invest. A bank might pay 5% on deposits and charge borrowers 7%, earning a 2% spread. If securitization reduces their funding cost to 4.5%, they can either lower rates for borrowers (expanding market share) or pocket the extra margin.

Investors gain asset class access they couldn’t get otherwise. A pension fund managing $20 billion can’t open retail branches and underwrite 50,000 auto loans. Securitization packages those loans into a $500 million bond the pension fund buys with a single transaction. They get diversification across thousands of borrowers, professional servicing, and liquid securities they can sell if needed.

Higher yields become available. In 2021-2022, when 10-year Treasuries paid 1.5%, subordinated tranches of ABS deals offered 5-7%. Investors hunting for income flooded into structured products, accepting more risk for those extra percentage points.

Lower borrowing costs can trickle down to consumers. When competition for securitized assets is fierce, yields compress. That savings can flow through to borrowers via lower mortgage rates or cheaper auto financing, though banks often capture some of the benefit as profit instead.

Risks and Drawbacks of Securitization

Securitization isn’t free money. The complexity creates vulnerabilities that have periodically blown up.

Credit risk doesn’t vanish—it just moves. Investors still eat losses when borrowers default. During the 2008 crisis, even AAA-rated tranches of subprime MBS suffered principal impairment. Diversification across 5,000 mortgages doesn’t help if all 5,000 were originated with shoddy underwriting in overheated housing markets.

Opacity hides problems until they explode. A corporate bond comes with financial statements, earnings calls, and SEC filings. A securitized product comes with a trustee report showing aggregate pool statistics but limited loan-level detail. Investors often outsource analysis to rating agencies rather than digging through collateral themselves. When assumptions prove wrong, surprises hurt.

Moral hazard festers when originators don’t keep skin in the game. The “originate-to-distribute” model broke down spectacularly in the mid-2000s. Mortgage brokers earned fees for volume, not quality. They knew loans would be securitized within weeks, so why worry about whether borrowers could actually repay? Post-crisis regulations now require 5% risk retention—originators must hold a vertical slice or the equity tranche—to realign incentives. But enforcement varies, and clever structures sometimes evade the spirit of the rule.

Prepayment risk whipsaws investors. Homeowners refinance when rates drop, paying off high-coupon mortgages early. Investors holding MBS suddenly get their principal back and must reinvest at lower prevailing rates. Conversely, when rates rise, prepayments slow. Investors expecting to be repaid in 7 years find themselves locked in for 15 years at below-market yields. This “negative convexity” makes MBS tricky to hedge.

Complexity breeds mistakes. Structuring a CLO requires dozens of specialists—lawyers, accountants, modelers, rating analysts, trustees, servicers. Each hand-off introduces potential errors. In 2008, some CDO managers didn’t fully understand their own deals. Documentation ran to thousands of pages, and even sophisticated investors relied on ratings rather than reading every word.

Systemic interconnections amplify shocks. When everyone owns pieces of the same securitized pools, trouble spreads fast. Bear Stearns failed because hedge funds it financed couldn’t meet margin calls on subprime MBS holdings. Lehman Brothers collapsed under $600 billion in securitization-related exposures. AIG sold credit default swaps on mortgage bonds without posting adequate collateral. One institution’s distress cascaded to others through securitization linkages, freezing credit markets globally.

Rating agencies failed catastrophically. Moody’s and S&P stamped AAA on tranches that defaulted within two years. Why? Issuers paid for ratings, creating conflicts of interest. Models assumed housing prices couldn’t fall nationally (they did—by 20-30% in many markets). Agencies competed for business by offering the most favorable ratings. Congress held hearings, but the agencies blamed flawed assumptions, not their own negligence.

Transparency gaps persist. Unlike stocks with real-time pricing, many securitized products trade over-the-counter with limited disclosure. An investor might not know their auto loan ABS has seen delinquencies spike until they receive a monthly trustee report 45 days after month-end. By then, the market has moved on.

The 2008 financial crisis showed what happens when these risks converge. Subprime lenders originated mortgages to borrowers with poor credit and little documentation (the infamous “NINJA” loans—no income, no job, no assets). Wall Street securitized them, rating agencies blessed them, and global investors bought them. When housing prices stopped rising, defaults exploded. Lehman failed. Bear Stearns vanished. Congress passed Dodd-Frank with risk retention requirements, enhanced disclosures, and stress testing mandates. Markets seized for months.

Real-World Example: Mortgage Securitization

Let’s walk through a practical scenario showing how a mortgage pool becomes a tradable security.

The setup: Liberty Home Loans, a regional mortgage company, has originated 600 home loans over the past eight months totaling $180 million. Average loan size: $300,000. Average rate: 6.75%, 30-year fixed. Borrower FICO scores range from 700 to 800. Properties spread across Pennsylvania, Ohio, and Indiana. All loans have full documentation—verified income, appraisals, title insurance.

Step 1: Liberty decides to securitize. Holding $180 million in mortgages on their balance sheet requires significant capital reserves. They’d prefer to redeploy that capital into new originations. They hire an investment bank to structure a mortgage-backed security deal.

Step 2: Due diligence and pooling. The bank reviews loan files, flagging 27 mortgages with documentation issues or higher risk profiles. Liberty keeps those 27 on their books. The remaining 573 loans ($172 million) pass into the securitization pool. A third-party firm re-underwrites a random sample of 50 loans, confirming quality standards.

Step 3: Creating the SPV. Liberty establishes “Liberty Residential Trust 2025-A,” a Delaware statutory trust. Liberty executes a true sale, legally transferring ownership of the 573 mortgages to the trust. Legal counsel issues opinions confirming bankruptcy remoteness. Liberty remains the servicer, collecting borrower payments in exchange for a 0.30% annual fee.

Step 4: Structuring tranches. The investment bank creates four classes of securities:

- Class A-1 (Senior): $137.6 million (80% of the pool), rated AAA by two agencies, 5.25% coupon, first-priority payments.

- Class A-2 (Senior): $17.2 million (10%), rated AA, 5.75% coupon, second priority.

- Class M (Mezzanine): $8.6 million (5%), rated BBB, 7.00% coupon, third priority.

- Class B (Equity): $8.6 million (5%), unrated, residual distributions.

Liberty retains the entire Class B tranche (5% risk retention per Dodd-Frank rules), putting their own money at risk to ensure quality.

Step 5: Marketing and sale. The investment bank pitches the deal to institutional investors. State pension funds and insurance companies buy $125 million of Class A-1, valuing the AAA rating and stable cash flow. Asset managers purchase $30 million of A-2 for slightly higher yield. A specialty debt fund buys $8.6 million of Class M, seeking the 7% return. Liberty holds $8.6 million of equity.

Liberty receives approximately $163.4 million upfront (the $172 million pool minus the $8.6 million equity they retain). After paying the investment bank’s structuring fee (around $2 million) and legal costs ($500,000), Liberty nets roughly $161 million—cash they immediately deploy into new mortgage originations.

Step 6: Monthly cash flows begin. The 573 borrowers collectively pay about $1.05 million per month in principal and interest. Liberty collects payments, deducts the servicing fee ($43,000 monthly), and wires the net $1.007 million to the trustee, Bank of New York Mellon.

BNY Mellon follows the waterfall:

- Pay Class A-1 its monthly interest ($601,000) and scheduled principal.

- Pay Class A-2 its interest ($82,500) and principal.

- Pay Class M its interest ($50,000) and principal.

- Distribute remaining cash to Class B equity holders.

Everything flows smoothly for 18 months.

Step 7: Defaults occur. Economic conditions deteriorate. Unemployment rises in Ohio. Over months 19-30 of the deal, 17 borrowers default. Liberty forecloses, recovers property through sheriff sales, and recoups 65% of outstanding balances on average. Total realized losses: $2.1 million.

The equity tranche absorbs the entire $2.1 million loss. Liberty’s $8.6 million stake drops to $6.5 million in value. Classes M, A-2, and A-1 remain unaffected—they continue receiving full interest and principal payments as scheduled. Rating agencies review the pool’s performance and affirm the AAA rating on Class A-1.

By year five, 85% of the original mortgages have been repaid or refinanced. The trust distributes final payments to remaining bondholders and terminates. Class A investors received every dollar owed. Class M earned their 7% coupon with no principal loss. Liberty’s equity stake, after bearing all defaults, returned about 6% annually—not the 12% they hoped for, but acceptable given the protection they provided to other tranches.

This example shows how securitization’s layered structure protects senior investors while concentrating risk at the bottom.

Securitization channels capital efficiently when transparency and accountability are maintained. But complexity without rigorous oversight invites disaster. Risk retention rules requiring originators to keep skin in the game aren’t bureaucratic red tape—they’re essential safeguards. Markets work best when the people creating products have real money at stake if those products fail.

Dr. Janet Yellen

Comparison Table: Common Securitization Types

| Type | What Backs It | Who Typically Buys | Risk Level | How Easy to Trade |

|---|---|---|---|---|

| Agency MBS | Home mortgages with government guarantee | Pension funds, central banks, insurance firms | Low—government covers losses | Very easy—huge, liquid market |

| Non-Agency MBS | Mortgages without government backing | Asset managers, hedge funds, some banks | Medium to high—no safety net | Moderate—smaller market than agency |

| Auto Loan ABS | Car loans and leases | Insurance companies, mutual funds, banks | Low to medium—cars can be repossessed | Easy—active secondary market |

| Credit Card ABS | Credit card balances | Money market funds, banks, asset managers | Medium—unsecured debt | Easy—frequent new issuance |

| CLO | Corporate loans to below-investment-grade companies | Hedge funds, insurers, banks, credit funds | Medium to high—depends on economy | Moderate—some tranches trade actively |

| CDO | Mix of bonds, loans, or other securities | Hedge funds, specialized credit investors | High—layered complexity | Hard—limited buyers |

FAQs

Securitization bundles loans—like mortgages or auto financing—into a package, then sells bonds backed by borrowers’ monthly payments. Banks get cash immediately instead of waiting years for repayment, while investors buy bonds that pay interest from those loan payments. It’s a way to turn future income into money today.

Banks free up capital fast, letting them make new loans without waiting for old ones to mature. They also transfer default risk to investors, reduce regulatory capital requirements (since securitized loans leave the balance sheet), and access cheaper funding from institutional investors compared to traditional deposits.

Almost anything with predictable cash flows. Common types: mortgages, auto loans, credit card balances, student debt, equipment leases, and corporate loans. More exotic examples include music royalties, aircraft leases, franchise revenues, and even future lawsuit settlements. If it generates regular payments, someone has probably tried to securitize it.

Depends on what tranche you buy and how carefully you evaluate the underlying collateral. Senior tranches with strong underwriting and credit enhancements offer low risk—you’ll likely get paid in full. Junior tranches can deliver high returns but may lose everything if defaults spike. The 2008 crisis taught investors that even AAA ratings don’t guarantee safety when collateral quality deteriorates across an entire market.

Massive role. Lenders originated subprime mortgages with weak underwriting, securitized them, and sold bonds globally. Rating agencies gave AAA ratings to risky tranches. When housing prices fell and defaults surged, trillions in securities lost value. Major banks failed because of securitization exposures. The interconnections meant losses spread system-wide, freezing credit markets and triggering the worst recession since the 1930s.

Mortgages have much longer durations—15 to 30 years versus 3 to 7 years for most other consumer loans. Homeowners can refinance, creating prepayment risk that doesn’t exist with auto or personal loans. Government-sponsored enterprises (Fannie, Freddie, Ginnie) dominate mortgage securitization, providing guarantees not available in other markets. Mortgage pools also tend to be larger—$500 million to $2 billion—compared to $100-300 million for typical ABS deals.

Securitization remains a core piece of modern finance, moving hundreds of billions annually through capital markets. It works well when underwriting stays sound, structures stay transparent, and originators retain meaningful risk. It fails spectacularly when those conditions break down. Understanding the mechanics—how loans become bonds, how risk gets sliced and redistributed, where vulnerabilities hide—matters whether you’re a banker structuring a deal, an investor evaluating bonds, or a borrower whose mortgage just got sold to a trust in Delaware.